Leaderboard

-

Guardian

Supreme User4Points1,970Posts -

Random Guy

Registered User2Points142Posts -

Hacker

Supreme User2Points2,077Posts -

SpeedOfHeat

Registered User2Points101Posts

(1).thumb.jpg.7759999c13b3f642753de813ad11dd09.jpg)

Popular Content

Showing content with the highest reputation on 05/29/2022 in all areas

-

4 points

-

2 pointsShe's got a thing for pilots. Remember her from "The Rocketeer?" Lord have mercy.

2 points

2 points -

2 pointsI prefer the original Kelly McGillis over the sequel Jennifer Connelly. Fight me.2 points

-

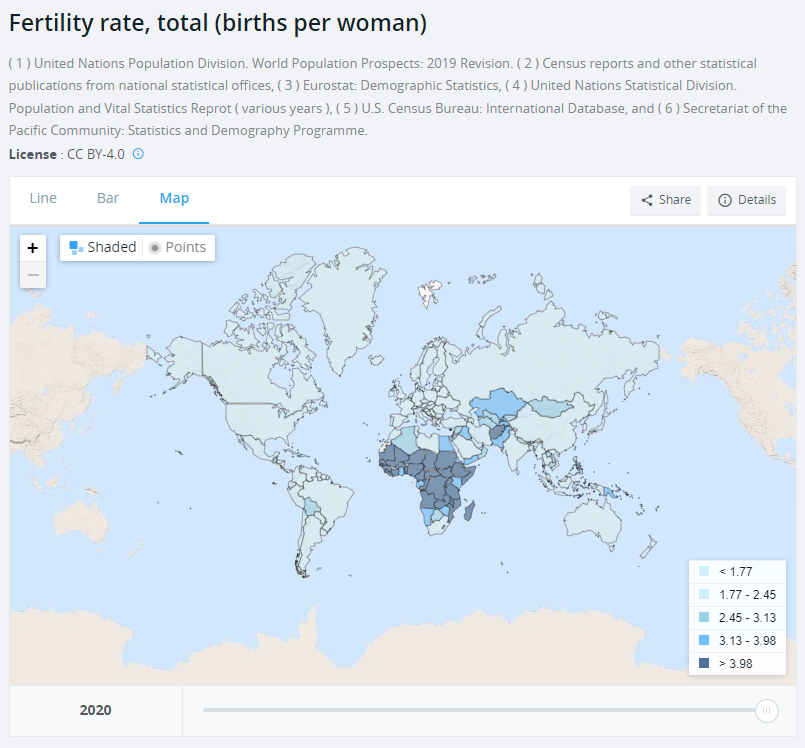

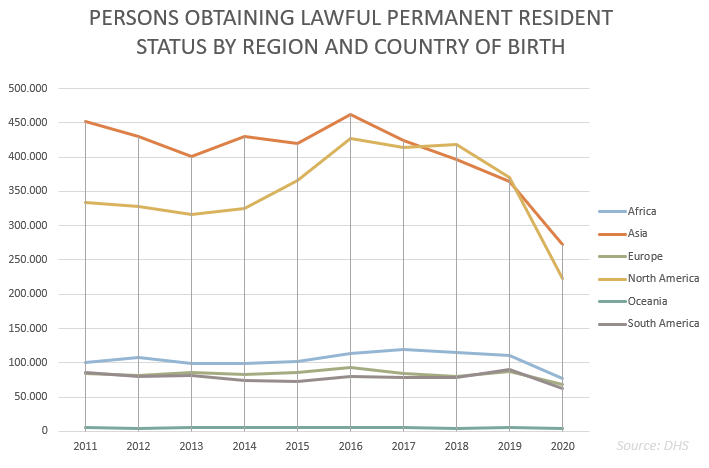

2 pointsThe birth rate in the US and the EU are approximately equal (1.6 vs 1.5), and the birth rate globally is mostly below replacement rate. The only place that doesn't hold is where birth control is not widely available, which is Africa. So in general, assuming developed countries want to continue to provide the same amount of goods and services to a nearly constant population over the next 20 to 50 years, they have to import some workers from Africa and other undeveloped regions. Hence why the EU accepted an influx of migrants from the ME & NA, despite the risks involved. However, immigration to the US is decreasing as well, as incomes & quality of life are no longer sufficiently higher there than in other parts of the so-called 'global south'. That is, prices of critical goods and services are too high to draw migrants or for households to have larger families. All this means is that the total share of income going to households is too low, or conversely, the share of total income going to the financial (banks, NBFIs) and non-financial sector (firms) is too high. This is a well know fact, and one of the reasons why the US recently implemented a subsidy for families with children, an acknowledgement that the current economic system generates an insufficient amount of bargaining power for domestic workers resulting in wages that are too low and overly reliant on credit (and hence interest rate conditions) to finance living. But the statements made that China will implode based on these conditions applies to all developed states, in that context, as all are experiencing the exact same thing: an inability to maintain a workforce that produces the current level of output using just the domestic population. But what's not being discussed is that given stagnating or decreasing population levels in all developed states, fewer total goods and services are required to sustain the population. We don't need more stuff. In that case, the problem isn't one of insufficient goods & services available for households leading to an implosion of the state. The problem is that the total capacity to produce goods and services is larger than the population it serves, which means owners of Capital (machines, factories, and methods of producing things) and owners of the corresponding financial assets (capital) face decreasing prices and lower monetary values for this wealth. This is known as a 'general glut' in economic parlance, one where the 'captains of industry (& their bankers finance)' are desperate for the prices of everything not to collapse.

2 points

2 points -

2 pointsThe Air Force doesn’t care about anything other than the strat on your OPR. I can guarantee that every aircrew member has done more and made more sacrifices than any nonner out there. We got into this mentality that everyone is the tip of the spear thanks to that tard Welsh, and won’t recover anytime soon. Sent from my iPhone using Tapatalk2 points

-

I’ll bite on #3. The community is still figuring out what it’s culture will look like as it builds its capabilities past those if legacy tanker platforms. This is more prevalent on the AD-side, where they purposely built the initial cadre with folks from 21+ different backgrounds to develop a diverse range of thought and tactical experience. On the ANG/AFRC side the community is largely prior KC-135 drivers. These things take time to work out.1 point

-

1 point

-

1 point1 point1 pointAlso gotta wonder if we would suck as bad as the Russians (in a REAL degraded environment).1 point1 pointFIFY. You’re not going back far enough. Hell, I’m probably not going back far enough.1 point1 pointElon Musk has been very vocal about population decline recently and I'm wondering if this is connected.1 pointI'm going to take a wild guess and say a lot of folks on here are too young to remember these guys.1 point1 pointDoing the mission does not matter. Having thousands of combat hours and dozens of air medals does not matter. Risking your life does not matter. Killing the enemy does not matter. The Air Force does not promote pilots for doing pilot things. The Air Force promotes pilots for doing things that they could hire people for minimum wage to do.1 point1 pointAnd we also know there won't be any debates. No surprise, Joe doesn't do contemporaneous.1 point1 point1 pointThere's nothing better than watching an O-6 stand in front of a room of graduated TOPGUN crew and explain to them that they have to fly low on the ingress to stay below the radar of the SAMs, and that their Super Bugs are "no match" for the 5th Gen threat. On the other hand, Jennifer Connelly is a massive MILF.1 point1 pointAbout 30 min into top gun I thought it was going to end up overhyped but damn, the end was awesome. Great flying scenes throughout. My wife, 9yr old daughter and 12yr old son all really liked it. Def see it in theater preferably a imax or Dolby.1 point-2 pointsI know what Kelly McGillis looks like now but this is still better than Penny

-2 points

-2 points