Leaderboard

-

ClearedHot

Administrator11Points5,183Posts -

JeremiahWeed

Supreme User10Points353Posts -

StoleIt

Supreme User5Points1,674Posts -

Sua Sponte

Supreme User4Points1,687Posts

Popular Content

Showing content with the highest reputation on 07/29/2022 in all areas

-

8 pointsDon't mean to hijack the thread, but like I said, I've got a few.......... Okay – quick one from way back at United in early 2001. 757/767 Captain at United with whom I’m flying a 4-day trip. The guy doesn’t wear an undershirt, has brought one shirt for the whole trip and by day 2 he reeks. At one point, we’re turning between flights and waiting for the pax to start boarding. One of the F/As standing in the flight deck doorway says, “Oh my, we may need to get this lav serviced before we go, it stinks”. I look at her while doing the sideways eyes toward the flight deck and tell her, “It ain’t the bathroom”. I finally have to ask him to use the hotel laundry service before the next day. Max altitude on a 767 is 43,100 (WTF? I dunno – ask Boeing) We’re light and cruising on the last hour of our BOS-SFO transcon at FL400. Captain Stinky decides he wants to explore the edges of the envelope since he’s never been above our current altitude. “Hey, see if center will give us a block altitude from FL410-430. I want to see how this thing handles the max altitude.” “Really? I’m pretty sure it’s gonna be just like it is here at FL400” (Let’s not do dumb things – K?) “Yeah, go ahead and ask them” Of course, I gotta put in a little dig just to make sure everyone else knows this is stupid…… “Center, United 123, the captain would like a block altitude from FL410 to FL430.” “United 123, unable” Oh, that’s too bad. Would have been so much fun. 🙄 On another turn, he pulls out a no-shit photo album with real pictures that had to be developed from film in an old-fashioned camera. More shit for some of you to google when you’re done learning about Jim Croce. In the magic photo album, he has a bunch of nudes that he’s apparently taken over the years. Tasteful, playboy nudes (no Hustler baloney spread shots) but still pretty weird. Again, not one to turn down a porn (sort of) invite, I take a look. I wasn’t sure I wanted to know who these women were or why they had agreed to this, so I just left that question unasked. But this album is the most important part of the story because it plays another part the next day. This is pre-9-11 and one of the reasonably young, fairly hot F/As comes up to visit for a while during cruise. We’re just shooting the shit when the Captain’s SA low light comes on and he reaches for “the book”. He swings it out of his pubs kit into view and my heart stops. Slow motion…..”Nooooooooooooooooooo!!!!!” 😧 In horror, I’m thinking “Please God no……… I like my new job………you clown, WTF are you doing.” I’m giving him the “cut” sign across my neck and wishing I was somewhere else when actually starts opening it up while saying…… “Hey, I’ve got a photo album with some nudes that I’ve shot, do you want to take a look?” Now, I can’t say that part of me wasn’t curious to see if she’d be into it. I guess that was the part of me that wasn’t worried about my multi-million-dollar airline career crumbling to dust at my feet. Maybe this is how the book started in the first place back when he was flying DC-8s, FAs were stewardesses and all hot, everyone dressed up to fly and meals were served on fine china. 🤷♂️ Luckily, she just gives a little smile and says, “Oh, that’s okay – probably not something that I’d be too interested in, thanks anyway.” But that was her cue to leave, never to return. Thanks, dumbass.8 points

-

6 pointsI think they kept it on the down-low and had a private celebration with their crew chiefs.6 points

-

4 pointsIMO, at this point, if she doesn't go to Taiwan now (for literally any reason) it will be such a PR victory for China. It will give them confidence that they can dictate US political travel in their AOR.4 points

-

2 pointsSurprised it wasn't posted yet, but happy 50th to the Eagle bubbas here. An amazing combat aircraft and a brilliant piece of American technology.2 points

-

2 points2 points2 points2 points2 pointsIsn’t this thread called “Lighten Up Francis!”? A little humor is needed. Comedy used to be all offending and no one got worked up over it. People need to chill out. Sent from my iPhone using Baseops Network mobile app2 points2 points2 points2 points"Most people do not listen with the intent to understand; they listen with the intent to reply." - Stephen Covey2 points1 pointWhat is causing this witch hunt? I’m purposely staying off that page for many reasons. While it does come across some of my feeds, the current bashing on finance is also pure gold right now.1 point1 point1 point1 point1 point1 pointAs proud as I am of being a proper single-seat, single-engine, single-tail fighter pilot… I can give respect where respect is due. You’ll never hear me say it out loud in a public forum or at a Flag, but I know Eagle drivers are goddamn good at their job, and I wholeheartedly hope they are my escort team lead on night 1, no matter the theatre. I am proud to be 4G4L with them - 4th Gen 4 Life!!! Happy Birthday fellas!1 point1 pointSo for a FedEx interview should I talk about worldwide sex odysseys as a perk or not?1 point1 pointThe next one takes place about 18 months before the Most Interesting Captain trip. I’m only 6 months on the 777 at the time and this latest Captain is absolutely notorious with the 777 FOs. Since I’m a relatively new arrival to the jet, I am uninformed and go into the trip “cludo”. The first leg is one of the worst in the system with an 0400 takeoff to fly almost 7 hours from MEM to Anchorage as a two-man crew. Toothpicks holding eyes open, I’m willing to listen to whatever in order to try to stay awake. I get an earful as Captain Player describes the full-scale domestic disturbance that played out the night before he left on this trip. Cops at the house, he’s detained, wife kicks him out, no idea if he’s got a place to live when he gets back – classic Jerry Springer shit. Jeez dude, that sucks – I hope it works out, etc. etc. You okay to fly this trip? He says getting away for a while is probably the best thing. I try not to spin the guy up more than he is, but I’m thinking if I was in deep serious with the old lady to the extent that the po-po are involved and my future habitation in my residence is in question, leaving town with her having free reign with the checkbook and every available attorney in the area has serious potential to end poorly. Whatever, his call. We limp into ANC and I don’t see him for the next 24 hours until we’re leaving for Narita. Not surprised he’s out of contact considering the shit storm he’s dealing with at home. We leave the hotel and he appears to be in high spirits. Another 2-pilot leg at 7:30 block, but the sun is up the whole way and we’re well rested. He’s still pretty bummed about the home situation but he’s been talking to the wife and she’s willing to listen. “I’m just worried about being able to see my kids. I really hope we can work this out, blah, blah.” A while later, we’re 4-5 hours into the north pacific crossing and he starts telling me about his plans for a “sex vacation” to Trinidad and Tobago. “Oh, dude, it’s awesome. You land and they show up in a Range Rover, take you to the compound and you pick your chick for the week out of a line-up. It’s just sex, food, booze by the pool for the week. All inclusive.” 🙄 I’m thinking – what happened to the guy worried about his kids and trying to reconcile with his wife? So, like a dumbass, I open my pie hole. “Do you think the sex vacation is the best idea considering all the shit going on at home?” “Oh…. Yeah…. Maybe you’re right. Maybe??? 🥴 After 2.5 days in Narita (where I saw this guy zero seconds), we spend the next few days and two flights banging around short haul in Asia. Over the course of those flights, I get schooled on every city in our system that offers any opportunity to pay for sex. “You gotta try Pasha’s in Cologne… Go to this place in Dubai, I think I have a card………I hope we get revised to go to Singapore. I’ll take you to the 4-floors of whores there. It’s awesome – the higher the floor the more expensive and hotter the chicks are. If you every have any questions about where to go, shoot me a text, I’ll hook you up.” Now I’m pretty sure why I’m not seeing this guy on any of our layovers. I feel like I’m flying with Jeckel and Hyde. I never know if I’m gonna get crazy sex monger or bummed out dad/husband trying to keep the family together. The other comical aspect of this guy is that I don’t think he owns a mirror – or at least hasn’t used one in the last 15 years. 👴 I think most of us who are getting up in the years have that occasional loss of SA where we forget that we are invisible to every chick under the age of 40?......45?.......50? Not sure where the cutoff is. We have our new super-power of invisibility and we just need to embrace it. The hot chick in the grocery store parking lot isn’t smiling at you because she’s interested. She either thinks you look like her dad, needs help cuz her car won’t start or is completely broke and might be willing to make your day for a hundo. This guy is 64 if he’s a day and he looks every year of it. Yet, he still thinks he’s Captain Player. He’s been part of the international travel scene for so long that he’s forgotten that the only reason he’s getting attention in Asia, the Middle East or Europe is chicks dig the size of his wallet 💰. He actually pulls up to the chick in the Ferrari at the stop light and gives her a wink thinking something might come of it, the whole time forgetting that he’s effectively sitting in the human equivalent of a mini-van. So, now we’re doing long haul from Narita to Paris. I get the pleasure of his company for almost 4-hours, then a break in the bunk and then almost 3 hours more. For the 4-hour stretch, sad dad shows up and starts lamenting his situation. “What am I gonna do?..... etc, etc.” I learn that his wife is Russian and she’s a dentist. They met on one of his trips, eventually got married and he paid to put her through dental school. I’m about full at this point, so I’ve got my nose buried in a book trying to look busy and give the occasional sympathetic response. A couple of hours into this, he suddenly hands me his phone and says “Check it out”. I take a look at the screen and see a still picture of a blond chick giving some serious oral attention to an enthusiastically engorged dick. Not one to decline the occasional porn offering, I look a bit more closely. As I’m realizing this has the look of an actual picture and not something downloaded, he says, “That’s my wife”………..pregnant pause as I look up…………”and that’s me” – with a big grin on his face. Dude……”Did you just show me your junk in full rage with no warning? That’s not cool”. 🤮 He loses the grin and says, “Well, we’re swingers and it’s just our thing.” I didn’t think you’d mind. Then he starts regaling me with swinger stories – how awesome it is to do some chick while same goes down on the wife, etc. All I’m thinking is I can’t wait to get to the bunk for the next rest period. Rest break over, I’m actually dreading getting back up on the flight deck in case Mr. Hyde is back. He is, of course, and starts showing me pictures and reading texts from of a bunch of Eastern Euro chicks that he’s been “sexting” with. Our trip ends in Paris after our current flight, with a deadhead home. As we sit in the hotel bar after arrival in France, now he starts asking my opinion about whether he should deadhead home to FL or take a flight to Baku, Azerbaijan so he can hook up with one or more of the chicks that have been sexting him. “So, the get back with the wife plan and concern for the kids…. Maybe put that on the back burner for a week or so in Baku? – I’m sure it’ll work out okay.” That seems to re-cage him and he decides to book a ticket home. I’d like to think I had a positive influence in the end, but it was a seriously bizarre experience overall.1 point1 point1 point1 pointFunny you should post that. Years ago, I'm at Carlos Murphys West in Tucson for a 4th of July soiree. I'm with another A-10 dude and somehow we end up taking to this liberal couple. When they find out we are Hawg drivers, the liberal chick says, "How can you gun down women and children." Well, if ever a softball question was tossed my way, that was it. Just like the movie quote, I replied "It's easy, you just don't lead them as much." The shocked looks on their faces was absolutely priceless. We also ended up drinking with a midget wrestler who was the regional distributor for Coors but that's another story.1 point1 pointYeah, I got some stories............ First, I’ll say (in my opinion) the FO’s job is to be a tolerant chameleon, when necessary, which is usually infrequent. When I was an FO, I did that pretty well. I’m not suggesting a Captain gets to bring all levels of crazy, non-standard BS to the trip. However, some of the stories of conflict I’ve heard are just as much the FO’s fault for being unwilling (as opposed to unable) to flex and just get along. The one thing you never do is take your issues to management. You don’t put a fellow pilot’s job on the line over a dispute of any kind. The first option is man to man, face to face. If you can’t solve it that way, then the next stop is professional standards with the union. Ratting someone out to the company is really bad form. The bottom line is, if you’re an FO, let shit go and chill. The entertainment value of some of these guys is top notch. You’ll miss out if you bail too early. I never kept a “list”. I usually heard about these guys after I flew with them. Then I’d usually be asking, why didn’t someone warn me about this guy? Trust me, they were all on everyone’s list if they had one. After 23 years of doing this, I’ve got some doozies. I’ll start with “The Most Interesting Captain in the World” Standard 2-week around the world 777 trip at FedEx. At some point in the first few days, Captain Fantastic informs me that at some point in the late 1990’s, he had the lead role as the Phantom in the Phantom of the Opera on Broadway. Before he could begin his performances, he “blew his vocal cords out”, needed surgery and lost the part. I know it may seem stupid in hindsight, but I had no reason to question this and wasn’t in the frame of mind to wave the BS flag. In fact, the first instinct I had was thinking my kids (all musical theater performers) were going to be excited to hear that I flew with someone who was almost on Broadway. Of course, I asked if FedEx had agreed to give him a leave of absence to do this since that’s kind of a full-time job with multiple shows daily. He explained all that away and we moved on. The next one was, as a high school student, he discovered some DNA thing that had the potential to cure cancer. He didn’t have a PhD after his name, so no one took him seriously and he didn’t get any credit. I don’t know shit about DNA and it was early in the trip so I was still in “gee whiz, that’s pretty interesting” mode. The days continued and I heard about him getting the Arch Bishop of his church fired over a sermon topic, being a studio musician for various famous performers (this guy’ s cool, that guy’s an asshole, etc.) and his 80’s band that toured with and opened for Journey. They had a record deal but their drummer quit to get married and it fell through. I asked about the band name, etc. and did some online research but no joy. But it was the 80’s and they didn’t make it, so why would the interwebs have anything? Still semi-clueless and not being much of a talker myself, I’m just plugging along – warning bells haven’t started yet. As a side note, one day he starts going off about the full body scanners in use around the world. His doctor has warned him in the strongest terms never to accept them since we would be scanned so much more often than the average traveler. No shit – less than 24-hours later, we’re going through security in Osaka at o-dark-thirty and they try to make us go through one of those things. Amazing. I’ve been through KIX hundreds of times over that last 15 years and never – not once – have I every had to go through anything other than the normal metal detector for crews. Of course, it’s an absolute shit-show. This guy is getting badge numbers and asking for supervisors and threatening job loss – the whole shooting match. Of course, the Japs are sucking air through clenched teeth, avoiding eye contact and in full disengage mode trying to deal with the cray-cray American. They eventually plug in the normal machine; we walk through that and go on our way. He had big plans to write the whole thing up and maybe he did. I never heard a thing about it after that. There used to be a well-known interview process at Delta involving a psychiatric evaluation. From what I understand, the doctor doing the interviews eventually took his own life. Apparently, back in the day, Captain Fantastic threw his hat in the ring with Delta and got interviewed. His ability to parry and counter this psychiatrist’s questions during the evaluation were so clever and unnerving that the doctor eventually gave up in complete frustration. It was not long after this interview that the poor chap did himself in. Yes folks, our Captain was in fact, fully responsible for the death of the Delta doctor. By this point in the trip, I was a bit numb to the whole thing and it had been so much that I wasn’t really paying that much attention anymore. But I wouldn’t say the lightbulb had come on over my head quite yet. I know – I’m a dumbass. I am a music fan though and while we were waiting for an ATC delay in Shenzhen, we got talking again. We’re sitting #1 by the runway waiting to be released and somehow Jim Croce’s name comes up. You know – the guy who sang “Bad, Bad Leroy Brown”. Yeah – I know some of you don’t know it. Fucking youngsters. Google it. It’s 70’s folk/pop music. But the point is, that our Captain decides to tell me that “I used to play with Jim”. Now my radar finally comes out of test and I’m starting to really scan. I saw our hero’s birthday on the Gen Dec multiple times that trip. The most amazing Captain was born in 1961. I knew Croce died in a plane crash in the early 70’s so I looked it up when I got to my room that night. 1973. Mutherfucker!! So, you played with ole’ Jim when you were 12, huh? Yup – he got me. I guess I try to take people at face value. But I gotta say, if I was still an FO, I’d fly with him again just for the entertainment value. I’d love to be able to egg him on and see how far I could get him to go. Point being, not all the crazies are worth avoiding. Think of all the stories you’d miss out on.1 point1 pointAnecdotal, but I was in Portland two weeks ago. Our copilot who was meeting us for dinner got spit on and chased by a homeless person. It was like playing frogger dodging all the tents and literal human pieces of shit to get back to our hotel. Also, literally just got back from SFO today and it wasn't as bad as Portland, but still tons of homeless everywhere and very dirty (granted, that might be the normal). Met up with one of my E's for dinner who moved there and he told me he sold his car so it would no longer be broken into (among other reasons). Ironically, my rental car got broken into last year at Fisherman's Wharf and all my personnel belongings taken (to avoid victim blaming: they were in the trunk, nothing in plain sight).1 point1 pointThis is the fundamental flaw in the entire ideology. If this was true we'd have no inflation. But we did have inflation, and that inflation will destabilize the societal faith in the system, which is a prerequisite to the functioning of the system. If faith in the system is lost, the system is lost. Watch what happens when the bond market decides to ignore. Money is a proxy for human output, period. If you increase the amount of money without also increasing the output (growth), you will eventually get inflation. The entire system of modern economic has been constructed to deny or disprove this reality, yet here we are. Between the Yen, the Eurozone bond divergence, and our own inflation, any suggestion that MMT or Keynesian economics are valid theories should be laughed out of the room. For my whole life the economists like Krugman have been trying to convince us that the laws of personal finance don't apply to macroeconomic systems. It's bullshit. The only difference is the time it takes to fall apart.1 point1 pointReading the Air Force Amn/NCO/SNCO Facebook page about finance is comedy gold! Highly recommend!!1 point1 point1 pointImagine sitting in that thing for 8+ hour missions on a regular basis. How much storage does that thing have for piss bags? The best solution was turning the Dornier into a do-everything platform.1 point-1 pointsNote I didn't say the system wasn't flawed. We can trace a drop of fuel through an engine without saying whether or not the engine is flawed. All systems are flawed, that's called entropy 😄. Whether or not its good or bad is another thing entirely. Whether or not the Fed and private banks can create money is different than money's effect on prices. Clearly, we can identify that banks create lots of money, and some of it is inflationary, and, some of the inflation falls into categories that people ignore (ex: asset price inflation, no one complains that house & stock prices are rising to the degree that gas prices are). Here is a chart showing the balance of Fed purchases (increase in gov money) relative to the US CPI: Money cannot be a 'proxy' for human output, because lots of human output, especially in services, is non-monetary in nature (ex: a mother's work producing children). Or, imagine a slave economy, where all output is produced by slaves and consumed by slave-holders, and that output has no price. The quantity of money and the quantity of output would be irrelevant to one another. Can we agree that banks are the source of money? Private and public banks are money creators, and this occurs when banks issue loans? I want to know where else money comes from, if this is not the only source.-1 points-1 pointsThe Fed has a mandate to control prices, but asset prices aren't included in that mandate. The Fed inflates asset prices, intentionally. Again, I'm not saying the Fed is good or bad, I'm trying to get at a good description of money creation in order to trace its path through the system, we're just trying to identify where the fuel comes from in the first place. And the Fed is one component of money creation, when it marks up the accounts of its account holders, who are banks. The private banks themselves create most of the money supply. Ok, here is a claim we can test. When a bank issues a loan, such as an investment bank, it would be interested in recouping the loan [principle + interest (risk) + inflation (expected)]. So any bank loan (money creation) would have included in it an adjustment for the inflation associated with not just this loan, but all loans, over the respective period of time. Is this adjustment for the change in total private bank lending over time (typically referred to as a 'credit impulse') reflected in bank loan documentation? Not that I am aware of. We can also look at the change to CPI or CPI + asset prices when defaults rise, because defaulting loans means that the corresponding destroyed money is never destroyed. During periods of cascading defaults (firesales) does the CPI or asset prices rise? No, typically both decrease. Next we can think about it from the perspective of a single loan for a business that purchases only labour, a single 'monetary circuit' (Graziani, pictured below). #1, the bank creates deposits for the firm, #2 the firm pays workers... [If all money is always inflationary, are workers wages rising? The wage contract is typically agreed to and fixed prior to payment]... #3 Workers buy and consume the output... [If all money is inflationary, are the prices for the produced goods increasing? I don't believe so, firms typically set prices equal to costs plus a markup and don't respond to immediate changes in demand. Plus, any inrease in prices means an inrease in inventory, which would mean losses for the firm and default because the workers don't have enough money to pay increasing prices for the output, they would need additional loans from the bank]... #4 The firm repays the loan destroying the money created by the bank. Where in this circuit are prices changing because 'all money is always inflationary'? Please see the chart I posted above, which shows the response of CPI to Fed QE operations (no correlation). I agree that the Fed causes a change in lending behaviour, and you are spot on about that increasing 'moral hazard' and potentially 'misallocating resources', and that the asset price inflation will likely reverse if the Fed attempts to unwind QE which is happening now. These are valid points--and I'm not trying to antagonize you, I like your analysis--but I want to purge from it a reliance upon commodity money first and foremost. Banks create money, gov and private banks, and they are the decision makers about where the path of our economy leads (what we make, what we consume, where its made, etc). And this is not neutral <-- not just some function of the highest rates of perceived return, but subjective decisions of imperfect people with power. I don't understand what you are trying to convey here. When I purchase milk at the store, I am receiving productivity because I am paying with money. But if someone gives me the same milk, I am not receiving productivity because no money is involved? In the case of 2LT copypaster the increase in productivity doesn't do anything to the price for his labour. His wages don't go down as a result of his productivity increase. Regardless, we don't need a theory of prices or inflation in order to trace a unit of currency through the financial system. We only need to agree on the origin and substance of money in the real world, which today comes from a bank and resides on bank ledgers digitally. Well, the Fed is not authorized politically to disburse deposits to households. They are fully aware of the impact of QE on asset prices, that was Bernanke's stated intention ('wealth effects'). But at the very least your statement here is agreement that bank money creation is not always inflationary--in the case of QE an equal amount of reserves was not destroyed, the Fed added reserves and has not taken them out yet. I think you must concede this point, and I will re-reference this chart, which shows Fed QE yoy change correlation with CPI change (no correlation of Fed printing to CPI): COVID reduced productivity, and reduced (constrained) supply through unforeseen bottlenecks, which has contributed to inflation in goods and services. The impact on globalization is unclear, but your speculation may be correct. But the 'irresponsible money printing' here is unclear--all money is printed, what makes some money responsible and some irresponsible? Again, genuine question, and keep in mind that banks regularly create money for increasing future output, in other words, that output doesn't exist today for purchase. And this is where I want to get to. Neoclassical economists do not have an empirically valid theory of inflation. Post-Keynesians do. And I posted about this earlier in the thread--the Fed paper which acknowledged Post-Keynesian theories of inflation and money. When we say that the central authority doesn't understand--THEY DO UNDERSTAND. They just want something very different from you, and they are getting what they want. Not just too much debt, too much debt which won't be repaid--unproductive debt. And, a big part of that is housing debt. Any debt which does not increase income is technically considered unproductive. All mortgage debt, consumer debt, is by that definition unproductive. Remember, when you say 'Keynesian' you are specifically referring to the school known as 'New Keynesianism', which isn't based on the works of Keynes! It's based largely on the work of Hick's and Solow, and known as Neoliberalism, a resurgence of classical economic ideas from the 18th century. The idea that money is an exogenous commodity. F--- the academics mate. Private debt levels and repayment capacity of constrained balance sheets matters. That's the point of all this. Everyone here needs to know how the system actually works. Trace the drop of fuel through the machine, trace the unit of bank money from creation to destruction--that way people can decide for themselves what policy is the best way forward.

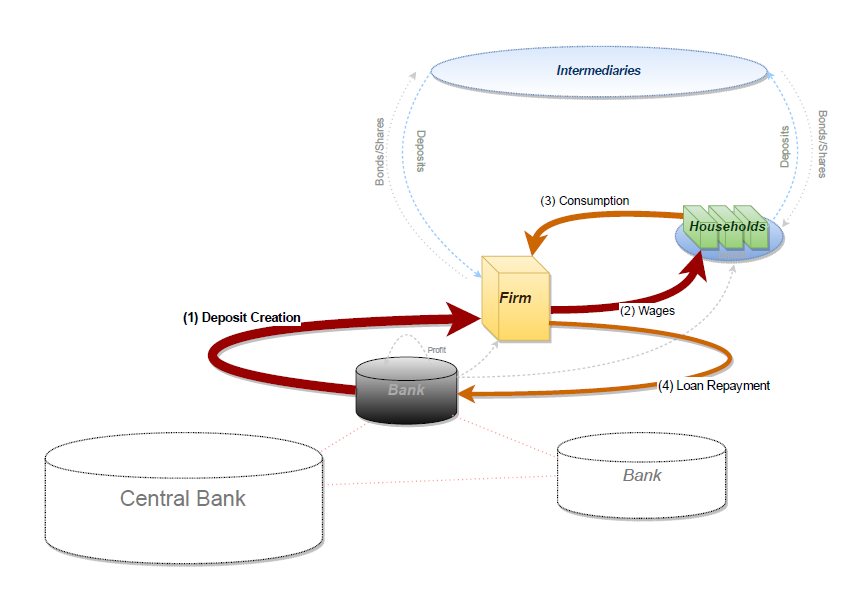

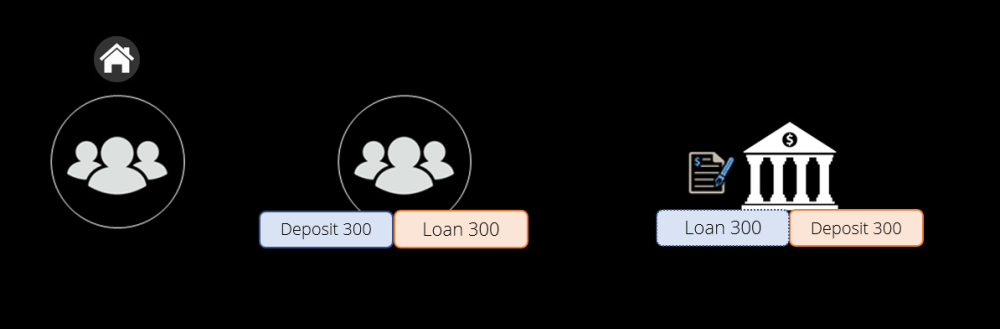

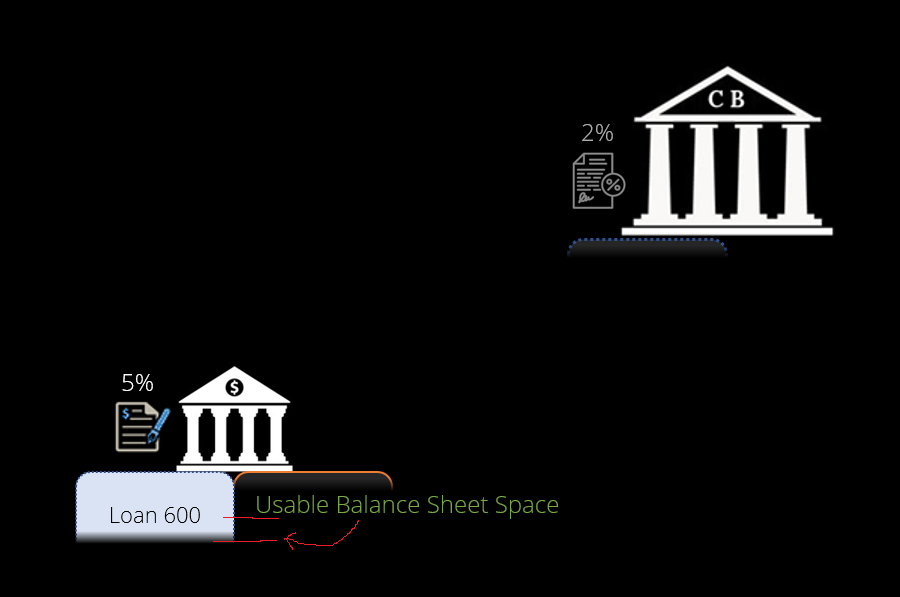

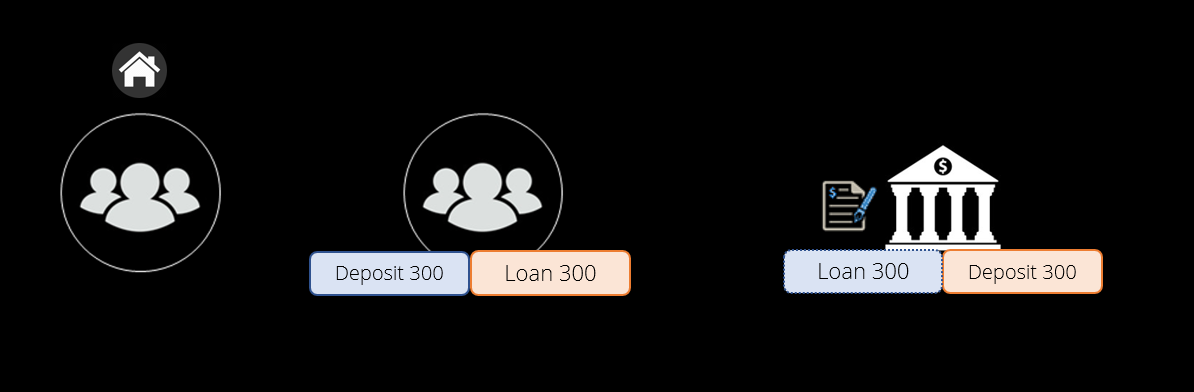

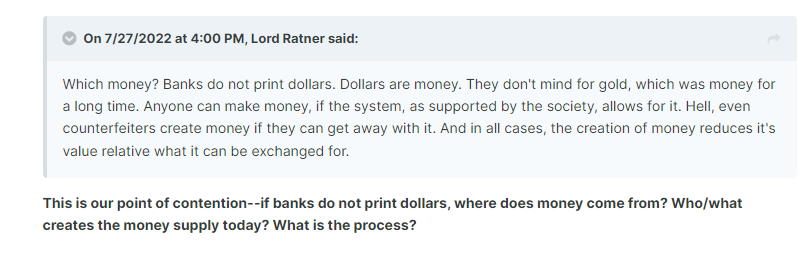

-1 points-1 pointsWhat is a mother paid for her product, the child itself? Nothing. Keep in mind that this output is the source of all future output, but women aren't compensated for it. Mothers are not paid for that labour. Do you pay your wife a wage, according to a contract, and does she negotiate her wages with you, subject to terms of law? This is not a reference to the southern US. Slave economies were the basis of social organization for thousands of years, beginning before the Sumerians themselves. This is our point of contention--if banks do not print dollars, where does money come from? Who/what creates the money supply today? What is the process? This is classical monetary inflation (too much money chasing too few goods) and this was refuted by the Fed. Inflation is not just a monetary phenomenon, and supply is not the only factor contributing to price changes. The paper is linked earlier. The platinum coin denominated as $1T would be produced by the mint and purchased by the Fed. The Fed would mark up the TGA by $1T and put the coin in a glass case on the wall. This is Rohan Grey's PhD paper, the source of this discussion topic, it's worth a read. Not sure how this relates to the financial system as it exists today. Similarly I don't think this would pass for a sufficient explanation of an aircraft system today either. Yes. The bank balance sheet expands, liabilities are created, those liabilities can be used for making payments. A loan is a legal contract, and exists within a legal system. All the effects and dynamics of law apply. The underlying collateral, if there is any, as private property, rights to use of property, all are affected. The IMF makes lots of dollar denominated loans to states that can't create dollars except through exports or asset sales that it knows won't be repaid, those loans have binding legal properties which are then wrought upon the debtor state--and that debtor cannot call the IMF and say 'hey, this isn't a loan sorry'. The US Gov won't 'pay back the debt', because in accounting terms that doesn't make sense. So long as someone has a desire to save, separate of the desires or behaviour of the private sector, the gov is the only entity which can swap an interest bearing note for those deposits. This is covered in detail via the animated slideshow linked earlier in the thread (screenshot above). If we trace the unit of currency through the financial system, the answer to your question becomes self-evident. You don't have to hear it from me. Here I think you mean that liabilities are being created and the corresponding asset has no market value. Or, in the case where the bank has positive equity, it can write liabilities to its ledger and create money--its not purchasing a loan contract from a borrower, its using the empty space on its balance sheet created from past loans and other loans (assets) currently on its books. Indeed, the deferred asset the Fed is creating right now demonstrates that money does not always need to be a loan, the Fed is just marking up its liabilities and assets without any contractual obligation applied to any human being. It's literally risk-free money for banks created from nothing. If you repay all loans, right now, using existing deposits, what happens to the money supply?

-1 points-1 pointsWhat is a mother paid for her product, the child itself? Nothing. Keep in mind that this output is the source of all future output, but women aren't compensated for it. Mothers are not paid for that labour. Do you pay your wife a wage, according to a contract, and does she negotiate her wages with you, subject to terms of law? This is not a reference to the southern US. Slave economies were the basis of social organization for thousands of years, beginning before the Sumerians themselves. This is our point of contention--if banks do not print dollars, where does money come from? Who/what creates the money supply today? What is the process? This is classical monetary inflation (too much money chasing too few goods) and this was refuted by the Fed. Inflation is not just a monetary phenomenon, and supply is not the only factor contributing to price changes. The paper is linked earlier. The platinum coin denominated as $1T would be produced by the mint and purchased by the Fed. The Fed would mark up the TGA by $1T and put the coin in a glass case on the wall. This is Rohan Grey's PhD paper, the source of this discussion topic, it's worth a read. Not sure how this relates to the financial system as it exists today. Similarly I don't think this would pass for a sufficient explanation of an aircraft system today either. Yes. The bank balance sheet expands, liabilities are created, those liabilities can be used for making payments. A loan is a legal contract, and exists within a legal system. All the effects and dynamics of law apply. The underlying collateral, if there is any, as private property, rights to use of property, all are affected. The IMF makes lots of dollar denominated loans to states that can't create dollars except through exports or asset sales that it knows won't be repaid, those loans have binding legal properties which are then wrought upon the debtor state--and that debtor cannot call the IMF and say 'hey, this isn't a loan sorry'. The US Gov won't 'pay back the debt', because in accounting terms that doesn't make sense. So long as someone has a desire to save, separate of the desires or behaviour of the private sector, the gov is the only entity which can swap an interest bearing note for those deposits. This is covered in detail via the animated slideshow linked earlier in the thread (screenshot above). If we trace the unit of currency through the financial system, the answer to your question becomes self-evident. You don't have to hear it from me. Here I think you mean that liabilities are being created and the corresponding asset has no market value. Or, in the case where the bank has positive equity, it can write liabilities to its ledger and create money--its not purchasing a loan contract from a borrower, its using the empty space on its balance sheet created from past loans and other loans (assets) currently on its books. Indeed, the deferred asset the Fed is creating right now demonstrates that money does not always need to be a loan, the Fed is just marking up its liabilities and assets without any contractual obligation applied to any human being. It's literally risk-free money for banks created from nothing. If you repay all loans, right now, using existing deposits, what happens to the money supply?

-1 points-1 pointsNothing about liberalism is compassionate. Treating individuals as labour inputs cannot be compassionate given basic properties of a human being, like family, community. CA purposefully under supplies housing because they don't want to live in a populated area. They don't want coastal CA to be like Hong Kong. If you mean that low interest rates drives up housing prices--yes, it does. But ultimately banks create the money they issue to home buyers, so house prices reflect whatever banks are willing to create. That's accounting convention--houses are priced according to comparables rather than some other metric, which produces a pro-cyclical dynamic: the more banks lend, prices go up, the more collateral prices go up, the more banks can justify creating money (larger loans). When the income of households fails to cover the interest burden, households take on short term debt to pay off their interest burden, which makes the system more susceptible to short term changes in interest rates. But the bubble dynamics of housing are much more complicated than that today, because the financial instruments themselves (MBS) serve as collateral for other money creation. A house of cards within a house of cards within a house of cards. This is why the Fed has placed itself in as a dealer in money markets via the Standing Repo Facility and Bond Purchasing program. Its has woven a web of interrelated debt structures which everything depends on but can't sustain itself. This is why @Lord Ratner is talking about there being 'too much debt', which is generally correct but an oversimplification--the wrong kind of debt (the wrong kind of money). Debt is money. You can't just reduce debt, that reduces money--the deficit reduction we see happening now may reduce the money supply far below the required amount needed to sustain the private debt structure.-1 points-2 points

-1 points-1 pointsNothing about liberalism is compassionate. Treating individuals as labour inputs cannot be compassionate given basic properties of a human being, like family, community. CA purposefully under supplies housing because they don't want to live in a populated area. They don't want coastal CA to be like Hong Kong. If you mean that low interest rates drives up housing prices--yes, it does. But ultimately banks create the money they issue to home buyers, so house prices reflect whatever banks are willing to create. That's accounting convention--houses are priced according to comparables rather than some other metric, which produces a pro-cyclical dynamic: the more banks lend, prices go up, the more collateral prices go up, the more banks can justify creating money (larger loans). When the income of households fails to cover the interest burden, households take on short term debt to pay off their interest burden, which makes the system more susceptible to short term changes in interest rates. But the bubble dynamics of housing are much more complicated than that today, because the financial instruments themselves (MBS) serve as collateral for other money creation. A house of cards within a house of cards within a house of cards. This is why the Fed has placed itself in as a dealer in money markets via the Standing Repo Facility and Bond Purchasing program. Its has woven a web of interrelated debt structures which everything depends on but can't sustain itself. This is why @Lord Ratner is talking about there being 'too much debt', which is generally correct but an oversimplification--the wrong kind of debt (the wrong kind of money). Debt is money. You can't just reduce debt, that reduces money--the deficit reduction we see happening now may reduce the money supply far below the required amount needed to sustain the private debt structure.-1 points-2 points

.JPG.d1814d984da67feb1e7014a05f8e66e5.JPG)

Account

Navigation

Search

Configure browser push notifications

Chrome (Android)

- Tap the lock icon next to the address bar.

- Tap Permissions → Notifications.

- Adjust your preference.

Chrome (Desktop)

- Click the padlock icon in the address bar.

- Select Site settings.

- Find Notifications and adjust your preference.

Safari (iOS 16.4+)

- Ensure the site is installed via Add to Home Screen.

- Open Settings App → Notifications.

- Find your app name and adjust your preference.

Safari (macOS)

- Go to Safari → Preferences.

- Click the Websites tab.

- Select Notifications in the sidebar.

- Find this website and adjust your preference.

Edge (Android)

- Tap the lock icon next to the address bar.

- Tap Permissions.

- Find Notifications and adjust your preference.

Edge (Desktop)

- Click the padlock icon in the address bar.

- Click Permissions for this site.

- Find Notifications and adjust your preference.

Firefox (Android)

- Go to Settings → Site permissions.

- Tap Notifications.

- Find this site in the list and adjust your preference.

Firefox (Desktop)

- Open Firefox Settings.

- Search for Notifications.

- Find this site in the list and adjust your preference.