Jon - Trident Home Loans

-

Posts

240 -

Joined

-

Last visited

-

Days Won

4

2 Followers

Jon - Trident Home Loans's Achievements

Flight Lead (3/4)

96

Reputation

-

You're good to apply now. The application doesn't expire and the credit report is valid for 120 days and just needs to be good through the closing date. Even for ones outside of 120 days I can just do a soft pull vs a hard pull. Application link below and my personal cell is 850-377-1114. The market is definitely a little weird with everything going on with the government. The bond market is down off it's highs in early Jan so right now we're at 6.125% with no discount points or lender fees on VAs with 720+ credit. Obviously hard to predict the future but it looks like we'll be seeing 5.99% at some point in the not too distant future. I think 5.75% is possible within your timeframe. All that to be said so often the "experts" think they know where the market is going it and get it completely wrong. If the 10yr treasury bond is moving down then mortgage rates are getting better. All that to be said we're still doing the no cost streamline refinances so we'll get you lower in the future without adding principle to the loan. Eric is an awesome realtor in ABQ. He's a retired herk Nav and super good guy. I closed an MC-130 pilot with Eric last year and enjoyed working with him. His cell is 505-306-0527 Cheers! Jon https://tridenthomeloans.com/jonathan-kulak/ jk@mythl.com

-

Hope everyone had a great Thanksgiving! Just letting everyone know that the new VA entitlement cap is out for 2025 going up to 806,500 from 766,550 for most of the county with higher limits in more expensive parts of the country. This means that all veterans have more entitlement available to get a second VA loan while keeping a previous home that's still on a VA. If you don't have enough entitlement to go zero down you can still get a second VA loan but there is a formula for determining the required down payment. This also means that if we do a no cost streamline refi for you and your loan amount is below 806,500 you'll get regular VA rates vs VA high balance rates which are a little higher. Don't worry, if you don't have a current VA loan outstanding then you can still go zero down without a limit as long as you qualify debt to income ratio wise. Happy to chat through any scenarios anytime! Enjoy the holidays! Jon

-

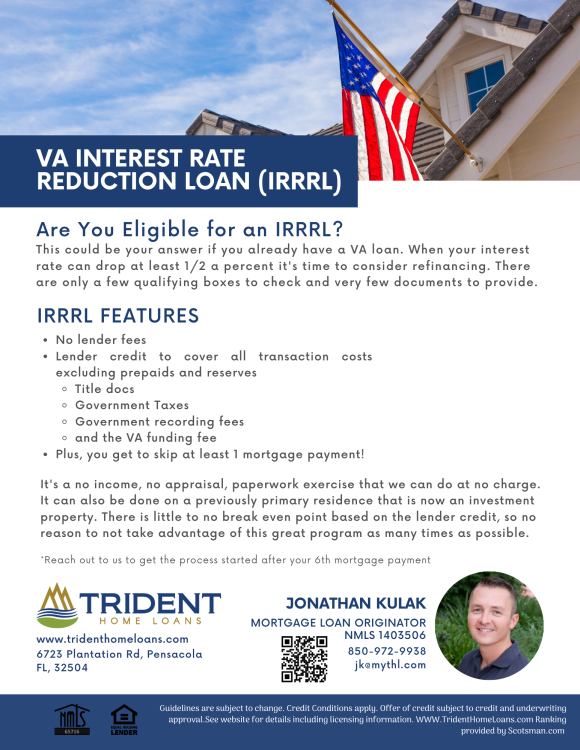

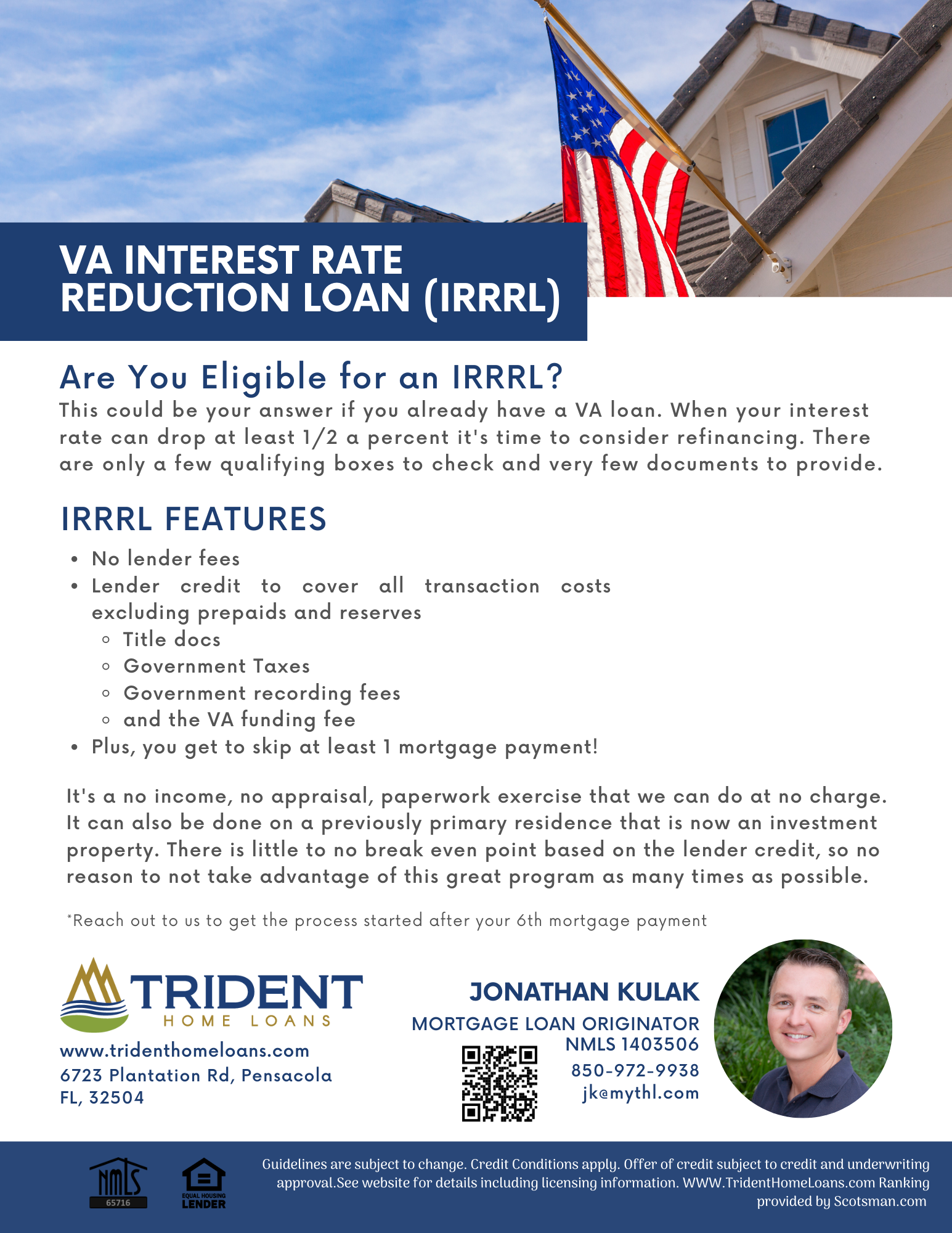

I don't pay to advertise or send out mailers but if any of you are sitting at 6.25% or higher on a VA loan that you've made 6 payments on with a loan amount under 766,550 I can drop you down to 5.75% at no cost (I'll pay all the transaction fees to include the VA funding fee) so you don't have a breakeven then we can rinse and repeat as rates go down. I can't do it in FL right now though cause the state taxes push the cost to high. No catches or fine print. If you have a loan above 766,550 give me a call and I'll take a look at what we can do based on your disability status or state you live in. When in doubt call me to check. We have a special pricing incentive for streamline refi's going but it ends on 3 Sept so hit me up sooner than later. Here is the website to knock out a quick app: https://tridenthomeloans.com/irrrl/ Feel free to call me on my cell...850-377-1114. Cheers! Jon

-

Thanks man! Congratulations again and thanks for trusting me with your new chapter in life! I’ll be here to knock the no cost refi out for you as rates continue their decline. Happy to chat purchases or no cost refi’s with any of y’all. Cheers! Jon https://tridenthomeloans.com/jonathan-kulak/

-

Thanks man! I’m always happy to help even if I personally can’t be the loan officer. I have a great team of loan officers who are licensed in states that I’m not and Marty our owner covers the rest. We’re still super competitive on our rates…especially VAs. Rates are moving in a good direction again and we only expect to see lower as the year goes on (assuming inflation reports are favorable). Expecting to do a lot of no cost streamline VA refi’s soon but purchases have kept us busy. Always happy to chat! Jon 850-377-1114 jk@mythl.com https://tridenthomeloans.com/jonathan-kulak/

-

We only lend on existing or new construction homes based on how we’re setup but land loans are definitely available through banks/credit unions. Usually 20% down on them. Market definitely continues to get more favorable. Reach out if you’re PCSing this summer or bought with a high rate. Jon

-

We do both conventionals and VA construction to perm loans. Not a big part of our business but it's something we can do if it helps. Jon

-

VAs are now in the upper 5s with no discount points or lender fees. Hit me up if you are purchasing soon or want to take a look at a no cost refi. Happy New Year! Jon

-

Wanted to pass a quick update since we’re entering the winter PCS season and there has been a lot of rapid improvements in the economy recently. Right now VA rates have come down fast out of the mid 7s to the low 6s and will be entering the upper 5s. Reach out if: you’re looking to buy and want to take advantage of our industry leading rates/no lender costs you’re under contract to buy at a 6.5% rate or higher you could still swap to use to get the lower rates and we can get the VA appraisal transferred over to avoid cost/closing delays. you already closed with a rate above 6.5% already and have made a few payments to do our no cost refi program where you don’t finance any extra principle into the loan cause we pay for the third party costs. The federal reserve announced yesterday 3 predicted rate cuts in 2024 but market futures expect 4-5. The fed is also estimating 4 in 2025 and 3 more in 2026 so rates will continue to decline and we can refinance you for free every 7 months without adding any cost or you having a refi breakeven point. Everyone will be refinancing so even if now isn’t the time don’t forget to get on my radar. We’ve done this no cost multiple refi strategy for years and it works out great for both you guys and for us. Our baseops clients helped build our business to a national leading lender over the years so I will always make sure you get treated the best. Happy to chat about anything/anytime (mortgages, real estate, airlines, or Cat E PIRR CAP-USAF jobs). Link to my website and also to our no cost refi program below. Merry Christmas! Jon Cell: 850-377-1114 jk@mythl.com https://tridenthomeloans.com/jonathan-kulak/ No cost streamline refi: https://tridenthomeloans.com/irrrl/

-

Assumptions are the best deal out there if you have the time and money to cover the gap between their balance and the purchase price. Mortgage servicers don’t staff their assumption departments well because there is not any money in it for them which is why it takes a long time. I know many of my past clients who have done assumptions but the story is always the same…takes way longer than you’d like, lack of communication/updates, and paperwork can be disjointed. It’s worth it in the end but keep your expectation level low going into it. Once you get into underwriting then the pace picks up. If it doesn’t work out we’re always here to help with a new loan and then we’ll do a no cost streamline refi for you next year as rates come down. Good luck! Jon https://tridenthomeloans.com/jonathan-kulak/

-

Definitely worth a phone discussion since there are a few variables to ensure a seamless closing...850-377-1114. Some general answer that’d help everyone… 1) Conventional conforming loans (not jumbos) with good credit can go up to 50% debt to income. VAs will go higher…I’ve had a 74% before. All lenders use the same automated underwriting systems so unless they have a self imposed restriction then everyone can go above 41% 2) VAs have the lowest rates usually by .5-.75% on 30yr loans. 15s are pretty similar. 3) You can do a simultaneous sale and purchase with both running in parallel and we don’t need to count the current home as long as it sells prior/we can get a copy of the signed closing docs 4) You can potentially qualify for a second VA loan not contingent on the sale of the current property but there are some VA entitlement numbers we need to run. 5) If you’re retiring or separating within 1yr then you need to build a plan because their are a lot of underwriting rules that apply that we can help you circumnavigate 6) Don’t pay off anything you don’t want to until we run automated underwriting because it may not be needed. Worst case we can exclude it and mark it paid at closing to save paperwork/energy on your part. 7) Preapproval apps don’t expire as long as income/assets don’t change. The hard pull credit report is only good for 120 days and needs to be good through closing but that can always be refreshed. A soft pull is an option but automated underwriting can’t be run off a soft pull so if debt to income is tight then a hard pull is the only way for us to determine what will work. Its always good to build a plan and there is no reason not to start sooner than later especially with major life transitions. Happy to chat anytime. Cheers! Jon 850-377-1114 jk@mythl.com https://tridenthomeloans.com/jonathan-kulak/

-

Thank for taking the time to write the great review and for trusting us again with your big life events! We're always working to keep our customer service level high and our rates low. I think we'll start seeing relief on rates next month after April's inflation data comes out which should start the slow decline of rates eventually back down to the 3.75%ish level that VAs like to sit at. The models predict mid to upper 4s by the end of this year with that continuing in '24-'25. We're already geared up to start doing no cost streamline refi's on VAs where we give a lender credit to wipe out the costs. Feel free to visit our website on the program and reach out if you're interest/want to get on the list. Cheers! Jon No cost VA refi: https://tridenthomeloans.com/irrrl/

-

This is one of those phone call scenarios because a lot of variables...are you AGR, ART, TR, Full Time, etc? Do you have a civilian job? How we qualify you and what documentation you'd need would depend on where you work, what your status is, where you want to buy, and when. As far as the disability if you're active duty your VA award date is backdated to your separation date so if you close before you separate it's unlikely you'd get the funding fee refund. Only way around that is to get a proposed memorandum of rating issued by the VA but I rarely see those play out. As a reservist, guard, or a vet who hasn't applied you'd definitely want to do an intent to file app. That buys you a year to get your actual app in, but once awarded they'd back date to your intent to file date plus backpay you. As long as you closed on a house after your intent to file date/aka the date they backdate to then you're eligible for the funding fee refund. I tell everyone who has separated/retired to do the intent to file JIC before they close if they don't have disability. Some people don't want to file or plan to but then decide later they do. Doesn't cost anything except a couple mins to do it and can get you/save you a lot of money. On our end you fill out a VA form that says you have applied for disability with the original initial docs we send you then we upload that to the VA. We then follow up with VA prior to closing to see if they have a proposed memo or an award to exempt you. If they don't then you close with the funding fee and once you get your backdated award the VA will automatically process the refund which will go into the account you have setup for direct deposit of your disability check. You can also call the VA regional loan center to initiate the refund process. There is a paragraph and phone number on the bottom of your VA certificate of eligibility explaining the refund stuff. I've seen it work out just fine for folks. Let me know if you want to talk more specifics offline. Jon 850-377-1114 jk@mythl.com

-

Thanks man! You’ll be in a good spot once you get the class date locked down. I think Trident is one of the few credible lenders out there that can speak/execute AD/reserves/airlines loans very well. There are some small broker shops that do but they don’t lend their own money or do their own underwriting. I always recommend folks transitioning add a mortgage plan to their 1yr out checklist if they plan to move. Once you are inside of 1yr from your separation date no underwriter for any VA, conventional or FHA can use that income because it’s not stable. There are ways to use future income or close you before your separation date is in but you gotta know the rules to work the gray area. I see other lenders preapprove people all the time based on their current AD income because they don’t check anything or are incompetent then it all comes falling apart in underwriting. Helped a guy who’s lender canceled them the day of closing because they did a final employment verification and discovered the separation date. Don’t fall for fancy sales tricks or being told what you want to hear. Always here to help! Jon

-

Thanks for the compliments from both of you! I enjoyed working with you guys and happy my team could provide such a great rate/service. I'm always here for you and I'll be keeping an eye out for no cost streamline IRRRL opportunities as rates decline! I've been meaning to post a market update on here since we're getting into PCS season. Also with all the crazy airline hiring we're doing a lot of loans for new hires or people upgrading so I'll address those too. Here are the highlights: 1) Mortgage follow the trend of the 10yr treasury bond not the federal reserve rate moves. The bond market as of today is down over 1% since it's high in Oct which means rates are down over 1% as well. The trend will continue through '23 with expectations that VAs will be back to the mid 4 area by the end of the year and then see continued decline back into the mid to upper 3s over the next couple years. Rates are definitely getting better and no cost refi opportunities are around the corner so reach out anytime if you want a sanity check. 2) If you closed Sept-Dec of last year you unfortunately hit the peak rates...reach out to me when you're making your 6th payment and I'll do a no cost VA streamline refi for you (informational flyer attached). No closing costs so no breakeven...then we do it again after you make another 6 payments as rates continue to decline. Anyone 5.5%+ will probably be able to take advantage of this by the end of the year. If you're 6%+ you'll be able to do it sooner. 3) Congratulations to anyone getting CJOs...so much hiring going on. Transition is a tough period when qualifying for a mortgage as is being on first year pay. I recently did a video (below) and had an article published in Aero Crew News (below) on airline pay that you can checkout. Every scenario is a little different so give me a call to chat through it. Pilot Pay Article: https://aerocrewnews.com/education-2/finances/mortgage/know-your-worth-pilot-mortgages-debunked/ Video: Bottom line is there is a lot of good stuff on the horizon and I want to help you however we can. Please feel free to reach out anytime. Cheers! Jon 850-377-1114 jk@mythl.com https://jonathankulak.floify.com/