Jon - Trident Home Loans

-

Posts

240 -

Joined

-

Last visited

-

Days Won

4

Content Type

Profiles

Forums

Gallery

Blogs

Downloads

Wiki

Everything posted by Jon - Trident Home Loans

-

You’re welcome and thank you! Sorry for the late reply I’ve been flying and kept meaning to reply. Always happy to help out a fellow airline/military guy. Great time to do an any type of mortgage. Definitely don’t hold back from calling us or lump us in with all the junk mail for refi’s that everyone is getting. We’re no pressure and straight forward...wouldn’t ever try to sell you something that wasn’t in your best interest. Only here to help...we make money by providing a great product and service. Not by charging fees or pushing you farther into debt. Jon 850-377-1114 jk@mythl.com

-

You're welcome! Elena did a great job as always. I still can't believe that local guy was over 1% higher than us. We see tons of quotes from lenders across the country and that was one of the worse. We usually beat everyone but that one was not even a competition. Thanks for trusting us to take care of you and your family! We're always happy to quickly sanity check any rates people are getting quoted without a mass of paperwork or credit pull. Jon 850-377-1114 or jk@mythl.com Sorry, no OH yet. Marty is pushing to get us licensed in as many states as we can over the next year, but it can be a slow process in some states. Banks are automatically licensed in every state. I'll ask around for a good OH lender referral for you. Amy is right on the funding fee stuff. Based on your scenario, you won't be able to get it refunded if you close on the refi before the disability award date next year. The VA is trying to push through claims if you're buying a house so that the award is prior to closing even if you can't get your check until after your official separation or retirement date. You can apply up to 180 days prior to separation/retirement which can definitely help people as they transition out and need to buy a house but want to avoid the funding fee. https://www.va.gov/disability/how-to-file-claim/when-to-file/pre-discharge-claim/

-

Thank you! That’s the goal every time! Glad you’re happy and congrats on the new place! Jon Quick money saving tip...a lot of people don’t know you can get free money from your realtor towards your closing costs. Not all realtors do it but some who don’t will match these programs cause they want your business. Some money is better than no money. Definitely worth checking out. There are probably more out there but we see these ones a lot. https://www.homesforheroes.com/ https://www.vrebnetwork.com/ https://www.usaa.com/inet/wc/bank_real_estate_rewards_network_main?akredirect=true

-

Anyone with at least 10% will still be exempt from the funding fee. Your exemption is in the top right corner of you certificate of eligibility. If it's not up there you can put in a application on e-benefits or we can do it through the VA portal. Normally it's updated when you are awarded. If you need to do the app all you need is a copy of the VA award letter. Cheers! Jon

-

It's somewhat addressed in the circular Amy linked to, but I agree it's not 100% clear yet. Basically the county limits that everything is currently based off will come back into play under the new rules if you're trying to do a 2nd VA will still having your 1st VA hanging out there. They also don't address in their examples if you can plus up the entitlement you have remaining by doing: (purchase price - entitlement remaining) x 25% down on the 2nd VA loan while still keeping your first VA. Hope that'll still be the case. Regardless if you sell and restore the entitlement you'll be back to the no max loan limit again, but the funding fee will go up to 3.6%. I'd definitely recommend trying to save for at least the 5% down payment option for any subsequent use purchases unless you have VA disability (then you're exempt). Cutting the funding fee down to 1.65% or 1.4% is a huge savings. Thanks Amy for getting this circular posted! Jon

-

Thanks 9! It was a pleasure working with you too! Glad we could improve the deal for you! Rates/pricing changes daily and sometimes multiple times during the day so always do a final check before you lock with someone. There can be a huge difference even in just one day. It's just like buying a stock on the market...Wall Street changes our pricing too. We will always give you the best deal we can when we go to do the lock and float you down for free if rates get better. Jon 850-377-1114 jk@mythl.com

-

Thanks for promoting us! You were definitely smart to do the IRRRL...saved you a nice chuck of change. We're flexible and IRRRLs are super easy on the borrower part anyway. Nothing like getting the original loan paperwork wise. We enjoyed working with you too! For anyone else interested...read my post from a couple days ago and if you want to explore it without any paperwork or commitment just send me (jk@mythl.com): 1) A copy of your last mortgage statement 2) Whether you have VA disability 3) Credit score Cheers! Jon 8503771114

-

Thanks! We were glad to help you flex between the two assignments...always a stressful time. We never charge you guys upfront for the appraisal like other lenders do. If you end up walking away or it doesn't close you don't pay for it. Just another Trident perk. Jon jk@mythl.com 850-377-1114

-

484,350. Gotta live in one of them to call it a primary residence and use the VA on it. That's just what the VA will "insurance", you can go above those limits and you just have to put 25% down of the difference between the purchase price and the limit. New rules on limits coming in 2020 which should be in your benefit so worth a relook once that guidance comes out. Jon

-

Thanks, man! That's the best compliment you could give me. We honestly want to help everyone save money and get the best deal. If what we have is not for your best interest I'll be the first to tell you. We don't buy mailing lists and spam people with trash advertising like all these other companies. We make money by saving you guys money. Marty, Tim and I were all military pilots and are all airline pilots now. We can help you guys better than anyone else that calls us because we all have the same background. Refi's are big right now because rates have come down so much. Some states are better than others to do a refinance...most of the cost for a VA IRRRL comes from the new title work and state taxes/fees. In the cheaper states, we can typically pay for all these costs for you so the refi can basically be "no cost" (not talking about rolling anything in, just our company paying it for you). The bigger the loan, the easier it is for us to cover your costs because there is more wiggle room. The other cost is the VA funding fee, but if you have VA disability you don't pay that. Again, depending on the size of the loan and in a cheap refi state we can even pay the funding fee in many cases. If you're sitting above 3.75% you should really take a look at doing a refi especially if we can cut most of the cost out. No reason not to be at or around 3.25% and skip a mortgage payment in the process if it doesn't cost you much of anything. We've even been doing VA jumbos at 3.25%. Here is a list of the 26 states we're licensed in order from cheapest to most expensive refi states based on new title work and state taxes/fees (based on a $300K refi). We can quickly figure if it's a smart move for you if you provide the following: 1) A copy of your last mortgage statement 2) Whether you have VA disability 3) Credit score No need for paperwork, sales pitch, or credit pull to run a rough estimate/assessment. If you like the numbers, then we'll do the formal stuff. If not, no harm or wasted time for you. Cheers! Jon jk@mythl.com 850-377-1114

-

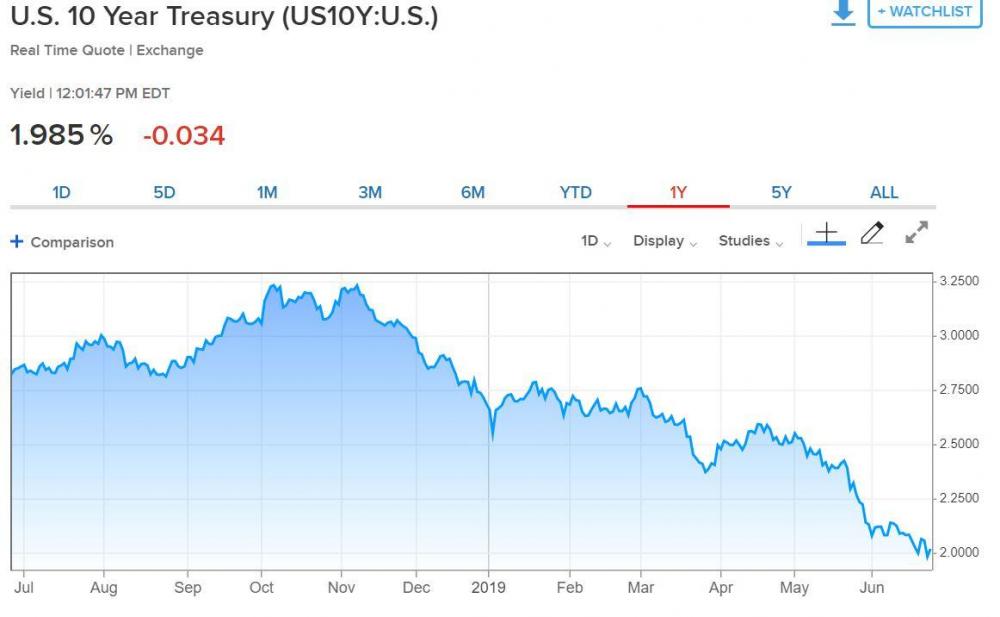

Thanks man! Congrats on finally getting into a place...long road but worth it in the long run. It was a pleasure working with you! Rates have continued to drop especially on VAs. Here is a snip of the 10yr Treasury bond today...mortgage rates follow it's trend. If you closed during one of the higher points you might want to consider a IRRRL (streamline refi). We have been doing them no-cost (we pay the closing costs and VA funding fee) and you just save money/skip one mortgage payment. No break-even point since we're covering the costs. Hit me up if you're at a 4% or more and have made 6 payments already or will soon to take a quick look to see if its worthwhile. No pressure if you reach out. Jon 850-377-1114 jk@mythl.com

-

Absolutely to doing a 20yr VA loan! The benefit to amortizing it as a 20yr vs doing a 30yr and paying like a 20 is the interest savings. I just used a file I was working on with a loan amount of 328K. Interest rates are essentially the same between a 20 and 30yr VA so the only difference is the loan time frame. If you did a 20yr and never made an extra payment you'd pay 118,512 in interest. If you did a 30yr and paid it off in 20yrs you'd pay 160,695 in interest. It's a common misconception that just paying it off earlier will make a 30 like a 15 or a 30 like a 20, but that's not really the case because of the fixed amortization schedule for mortgages. The best way I describe it is for every extra payment you make you're paying the loan off backwards...you're paying payment 360, 359, 358, etc. Those payments save you virtually no interest because all the interest is front loaded. Will you save money if you pay off your house early...absolutely, but you'd save more if the loan was amortized over a shorter period of time for the start. 15yr and 20yr mortgages are a lot of extra money to commit to every month so many people do the 30yr and pay it like a 15 or 20...definitely not trying to talk anyone out of that...just a little education on how the math really works. Cheers! Jon Cell: 850-377-1114, jk@mythl.com

-

Thank you all very much! It was definitely a pleasure helping all of you and congrats on the new houses! We're still locking at a 2yr low in rates and no-cost refinances are also taking off again. Give a ring, text or email if you want to see what we can do. Also if you're in our area (Pensacola) on 15 Jul we've got free tickets to the Wahoos military night for any of you. Jon jk@mythl.com or 850-377-1114

-

Thanks man! We’ve enjoyed working with you too! Thanks for helping to spread the word! We want to help people get the deals they deserve. Even if they don’t use us please keep telling your bros in the sqdn to shop around. Veterans United and USAA do 400k+ VA loans a year (#1 & 2 in volume according to the VA) yet they have the highest rates in the country.

-

Thanks man and congrats on the new house! It was a pleasure working with a sharp guy like yourself (obviously, you also fly for the world's best airline). We don't always get everything right and there can be bumps in such a complicated transaction, but we always own it and will do whatever we can to make it right. Marty (the owner) learned a long time ago that even eating the cost of a mistakes always turns out as win in the long run because we earn trust and loyalty through it which pays dividends in the future. We care more about the relationship than the one time transaction. Great rates/deals and great customer service is the business model. For everyone else, yesterday (18 May) we hit a 1yr low in rates so now is a great time to get a mortgage or think about doing a refi if you have a VA. You have to have made 6 payments and 210 days elapsed between the first payment and closing on a streamline VA refi (IRRRL) to close you, but we were locking 30yr fixed VAs with loan amounts under 484,350 with good credit at 3.375-3.5% with no points/fees. We can also work the rate to give a lender credit to pay up to all the refi closing costs so there is no break even point for doing one. Only other catch is we have to be able to lower your rate by at least .5% to do the IRRRL per VA rules. Feel free to hit me up if you'd like to look into it and see if it'd make sense for you. Jon jk@mythl.com Cell: 850-377-1114

-

I think you're just saying nice things because we're both Aggies;) Thank you Sir! I enjoyed working with you too! Elena made the magic happen though. Glad we could lower your monthly and keep the costs to do it low. TX is a good refinance state because they don't have a state/county taxes on real estate transactions. Let me know if you need anything in the future! Gig 'em! Jon 850-377-1114 jk@mythl.com

-

Thank you! Glad we could get you and your big family out of the RV and into the house faster! It was all Bri and Lisa making the faster closing happen. I passed along your thanks to them. Enjoy the new house and assignment! Side note: We get a lot of questions on getting a second VA loan if you still have your first one. Yes you can do it but it might require a down payment if you don’t have enough VA entitlement remaining. You need to know the county loan limit and how much your first loan was originally for. How much entitlement left formula: County limit (usually 484,350k) - original loan amount = remaining entitlement https://www.fhfa.gov/DataTools/Downloads/Documents/Conforming-Loan-Limits/FullCountyLoanLimitList2019_HERA-BASED_FINAL_FLAT.pdf If that covers your new purchase price then no down payment is needed If you don’t have enough entitlement left then: Second VA down payment formula: (Purchase price - remaining entitlement) x 25% = down payment By putting down 5% on a second time use VA you lower the VA funding fee from 3.3% to 1.5% which is a huge savings. The 25% missing entitlement down payment counts towards the 5% so you can kill two birds with one stone. Hope that helps everyone! Jon Cell: 850-377-1114 jk@mythl.com

-

Thank you and you're welcome! Glad we could help buy your first house mostly pain free! You're spot on about rates going down. Rates have been on a serious decline since the Fed announced last week that they were going to be doing an unexpected round of bond buying starting in May. If you're getting anything above 3.5% no points no fees on a VA under $484K or 3.875 on a VA jumbo then you definitely need to shop around. It's a great time to get a mortgage or do a refinance. Friday we hit a 15 month low on rates. Cheers! Jon 850-377-1114 or jk@mythl.com

-

Thank you Fud! It was great catching up with you and getting to help a fellow Aggie! Glad we made in painless for you! Enjoy the new house! Jon Cell: 850-377-1114 jk@mythl.com

-

Good news, we just got our NC, SC, AR and KY licenses approved in time for PCS season! We’re now licensed in: AL, AR, CA, CO, DE, FL, GA, IL, IN, KY, LA, MD, MI, MN, MS, NC, NM, OK, OR, SC, TN, TX, UT, VA, WA Let us know if you need any help or want to talk through a scenario or two. Cheers! Jon 850-377-1114 jk@mythl.com

-

Thank you so much! Glad we made it easy for you...that’s always the goal! Serena is awesome! It was a pleasure working with y’all! Congrats again! Jon 850-377-1114 jk@mythl.com

-

Thank you for the compliments and congrats again on the new house! Even more congrats on escaping Clovistan! Glad it all worked out so well. Having a good team working on your behalf makes all the difference. Serena is definitely a great realtor who stays on top of her work which makes our lives so much easier. I highly recommend her as well for anyone moving to the Hurlburt, Eglin, or Duke area. Jon 850-377-1114 jk@mythl.com

-

Thank you! You made it easy for us too! The recent wild market ride has really helped drive down rates so now is a great time to lock. If you’re getting quoted higher than 4.125-4.25 (4.55 APR) on a non-jumbo VA 30yr fixed, no points or 4.375 (4.625 APR) on a VA jumbo with no points you should consider shopping around. Thanks to a few of you guys asking, we got our AR and KY licenses submitted for and we also have the ball rolling with NC and SC. Expecting to have them by early 2019. Currently: AL, CA, CO, DE, FL, GA, IL, IN, LA, MD, MI, MN, MS, NM, OK, OR, TN, TX, UT, VA, WA Jon jk@mythl.com

-

Southwest publishes on the 10th. You can then start trading/giving away trips with other pilots and picking up new trips to improve your schedule. You can also trade trips with the company starting on the 25th. Most people don’t fly the schedule they receive on the 10th, but it’s up to you. There is a lot of scheduling flexibility in our contract. Sent from my iPhone using Tapatalk

-

Thank you! Bri and Lisa are the real brains behind the operation. They do a great job handling all the paperwork and smoothing things over with the underwriters. Serena is a great realtor and her husband is also retired AF/airline pilot so they definitely get the unique military/pilot challenges. I'd highly recommend Serena to anyone PCSing to Hurby or Eglin. Hit me up if you want her contact info. Jon 850-377-1114 jk@mythl.com p.s. I wrote another article for Aero Crew News on interest rate myths if anyone is interested (page 26-27) https://www.aerocrewnews.com/acn/2018/11-ACN-Nov-2018.pdf